Progressive Leasing: A Juggernaut Hiding in Plain Sight

Progressive Leasing: A juggernaut hiding in plain sight

Aaron’s holding company is masking the extremely cash-generative, third-party leasing business

Progressive has strong margins with operational leverage and generates significantly more cash from operations than earnings

Clear catalyst in sight - spinoff will unlock significant upside and multibagger potential depending on valuation of legacy brick-and-mortar business

Operational leverage cuts both ways and growth limited by capital in business (financial business)

Aaron’s is planning a spin-off of its third-party leasing business, Progressive Leasing, which has surpassed the traditional brick-and-mortar business in growth and quality. Aaron’s retail footprint classically relies on locations to lure customers and transact by providing “rent-to-own” options to households with poor or no credit. Progressive Leasing scales the economics of rent-to-own across third-party internet retailers and storefronts (i.e., Lowes Home Improvement, Best Buy), and then injects steroids to amplify the effects.

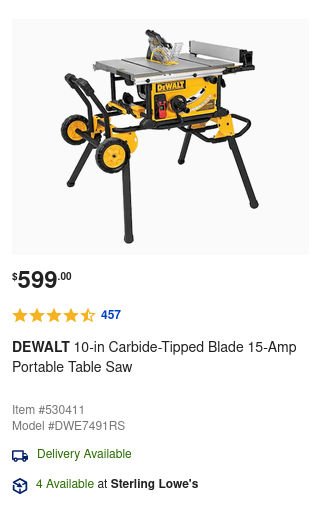

Progressive only does 12 month leases and effectively charges more than 100% in interest. Take this example leasing-to-own a DeWalt Table Saw from Lowes.

The shorter lease period lowers risk and allows Progressive to recoup capital used to purchase saw just after 6 months. The higher implied interest rates boosts returns on assets which are even more impressive since no stores are required to be maintained or stocked. The inventory is never actually touched by any employee of Progressive and yet they derive a majority of economic benefit from the transaction. The kicker is cash flow will likely always be higher than reported earnings due to depreciating leased merchandise on their balance sheet (even though they never touched it!). This means Progressive is an asset-light, cash gushing machine hidden inside a holding company with struggling retail footprint. Here is simple model:

The thesis here is Progressive is an exceptional business being masked by a more capital intensive company, and there will be extreme re-rating in shown cash flow and earnings post split. This should lead to a subsequent boost in P/E. This is warranted due to Progressive’s superior business and large Total Addressable Market (est $23B by Aaron’s management). Even if that is way off, there is still a lot of runway for leasing to work its way into other retailers in-store and online.

The big risk here is Progressive stops growing and revenues decrease. There is a significant amount of operational leverage in the business meaning profits and cash flow will substantially fall on lower revenues.

I haven’t found the Form 10 yet, so I am buying half position now and then diving deeper after figuring out separation details.

Comments

Post a Comment